Teaching guide: Elkington's triple bottom line

Highlights that businesses may have different objectives, not just profit.

Model/theory

Key points

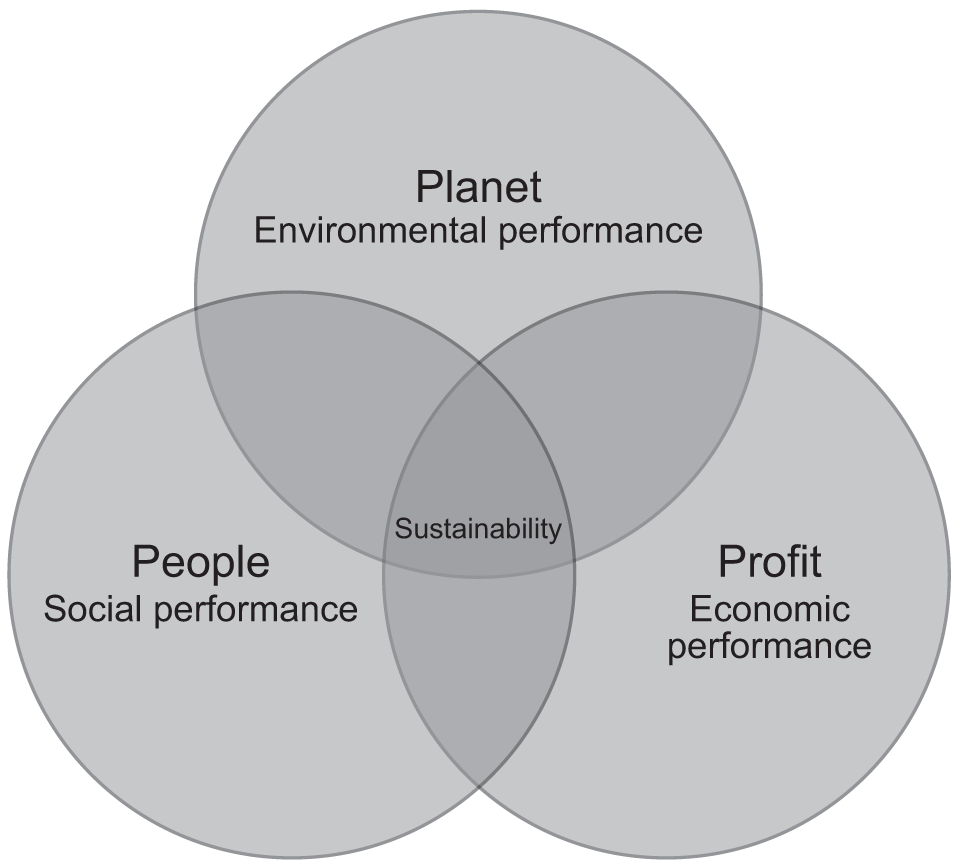

The Triple Bottom Line was a phrase introduced by John Elkington in 1994. The model highlights that business performance may be measured in a number of ways: in relation to its finances, its environmental impact and how socially responsible it is in relation to employees.

Elkington argued that only a company that was measuring performance in all three areas was measuring the full costs of its activities. The significance of this is that if you measure all these areas employees are likely to pay attention to them and change their behavior accordingly (rather than just focusing on profit).

However, in reality it can be difficult to find or agree ways of measuring the impact of business on the planet and people.

When you can use this

When discussing objectives, Corporate Social Responsibility and the social environment you could consider what factors might influence the objectives a business sets and why more businesses may be setting objectives linked to the planet and people as well as profit in recent years.

Where it's been used

Q23, A-level paper 1, 2017